해당 자료는 전북대학교 이영미 교수님 2023고급시계열분석 자료임

############## package library (forecast) #ses library (data.table)library (ggplot2)library (lmtest) #dwtest library (TTR) #SMA library (lubridate)library (gridExtra)

Registered S3 method overwritten by 'quantmod':

method from

as.zoo.data.frame zoo

Loading required package: zoo

Attaching package: ‘zoo’

The following objects are masked from ‘package:base’:

as.Date, as.Date.numeric

Attaching package: ‘lubridate’

The following objects are masked from ‘package:data.table’:

hour, isoweek, mday, minute, month, quarter, second, wday, week,

yday, year

The following objects are masked from ‘package:base’:

date, intersect, setdiff, union

1

# 데이터 불러오기 <- scan ("mindex.txt" )

\(S_n^{(1)} = w \sum_{j=0}^{n-1} (1-w)^j Z_{n-j} + (1-w)^n S_0^{(1)}\)

<- function (z,w,s0){<- c ()1 ] <- w* z[1 ] + (1 - w)* s0for (k in 2 : length (z)){<- w * z[k] + (1 - w)* Sn[k-1 ]return (Sn)

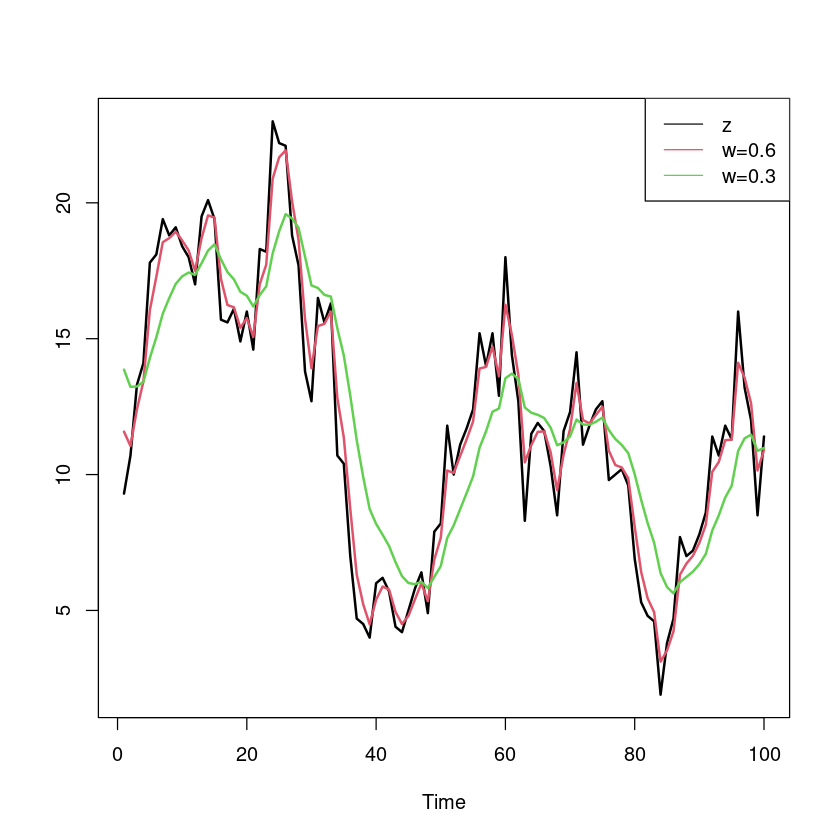

.6 <- simple_exp_smoothing (z,0.6 ,15 ).2 <- simple_exp_smoothing (z,0.2 ,15 )

ts.plot (ts (z), ses_0.6 , ses_0.2 , col= 1 : 3 , lwd= 2 )legend ("topright" , legend = c ("z" ,"w=0.6" ,"w=0.3" ), col= 1 : 3 , lty= 1 )

W값이 클수록 원 데이터와 비슷하고, 평활 효과가 작아진다.

W값이 작을수록 원데이터를 천천히 따라가고, 평활 효과가 커진다.

\(\hat Z_{t-1}(1) = S_{t-1}^{(1)}\) 이므로

<- c (2 ,3 ,99 ,100 ).6 [point-1 ].2 [point-1 ]

11.58 11.052 12.6262842848221 10.1505137139288

13.86 13.228 11.4677321254815 10.8741857003852

2

(1)

추세가 있기 때문에 이중지수평활법을 사용한다.

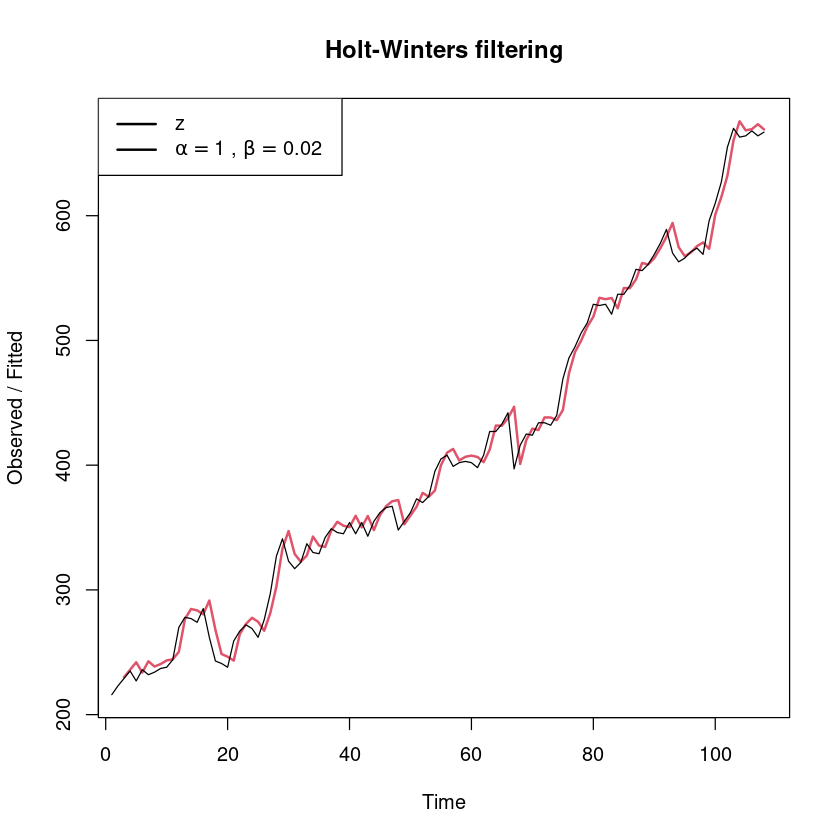

<- HoltWinters (z, gamma = FALSE )

Holt-Winters exponential smoothing with trend and without seasonal component.

Call:

HoltWinters(x = z, gamma = FALSE)

Smoothing parameters:

alpha: 1

beta : 0.01666631

gamma: FALSE

Coefficients:

[,1]

a 667.000000

b 5.145043

plot (female_smoothing, lwd= 2 )legend ("topleft" , legend= c ("z" ,expression (alpha == 1 ~ "," ~ beta== 0.02 )), lty= 1 , lwd= 2 )

- 예측오차 분석

head (female_smoothing$ fitted)

A Time Series: 6 × 3

3

230.0000

223

7.000000

4

235.9833

229

6.983334

5

241.9669

235

6.966945

6

233.7175

227

6.717501

7

242.7555

236

6.755542

8

238.5763

232

6.576287

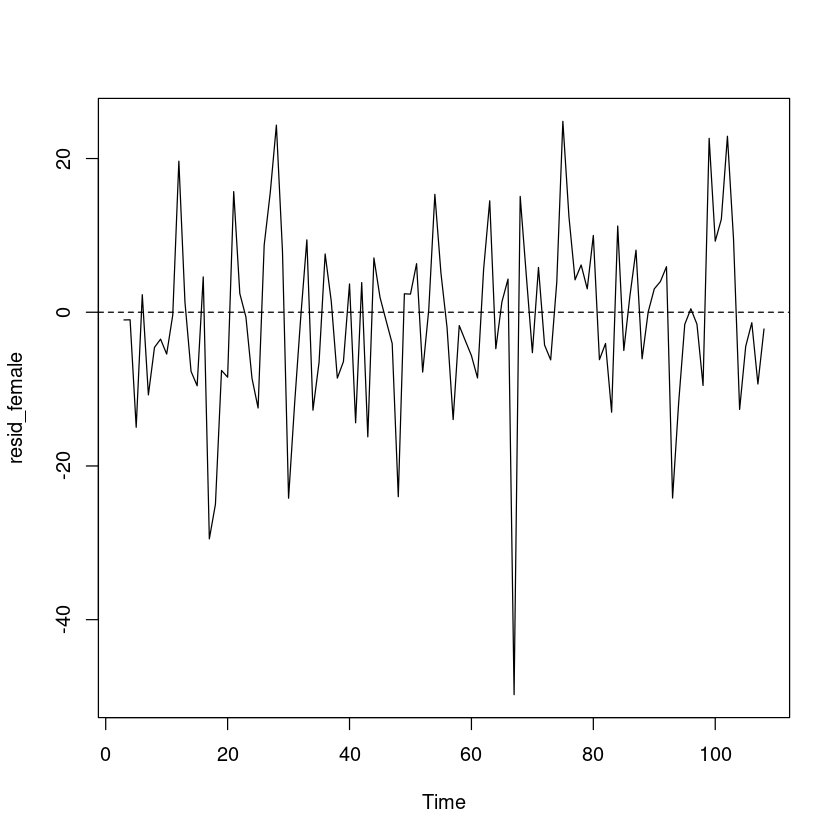

HoltWinters 함수를 사용하는 경우, 이중지수 평활값이 3번째부터 구해진다. 따라서 예측오차 역시 원데이터의 3번째 값부터 구할 수 있다.

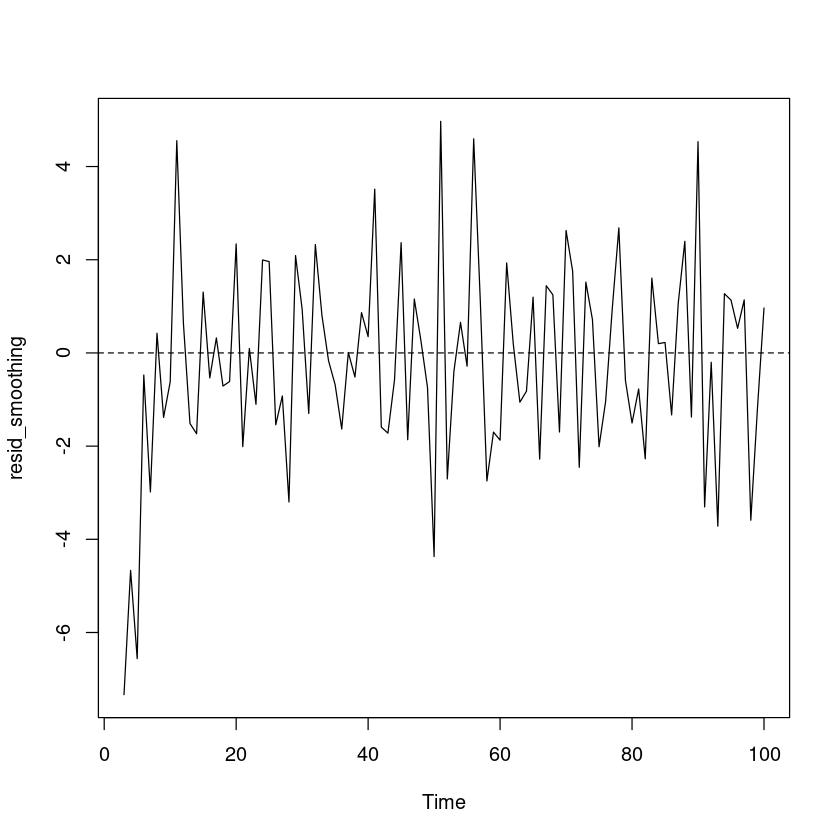

<- z[- (1 : 2 )] - female_smoothing$ fitted[,1 ] #또는 <- resid (female_smoothing) #같은 방법임

plot.ts (resid_female)abline (h= 0 , lty= 2 )

예측오차의 경우 0을 중심으로 대칭이고, 이분산성은 없어 보인다.

One Sample t-test

data: resid_female

t = -0.93497, df = 105, p-value = 0.3519

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-3.276746 1.176749

sample estimates:

mean of x

-1.049998

t-test 결과 예측오차의 평균은 0이라고 할 수 있다.

:: dwtest (lm (resid_female~ 1 ), alternative= "two.sided" )

Durbin-Watson test

data: lm(resid_female ~ 1)

DW = 1.7861, p-value = 0.2662

alternative hypothesis: true autocorrelation is not 0

(2)

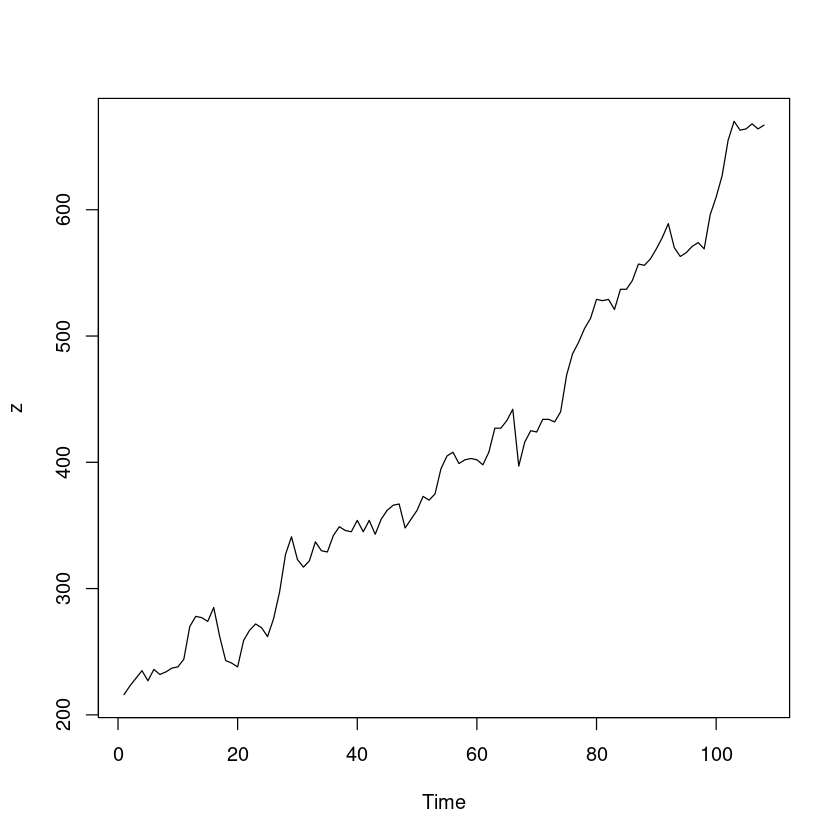

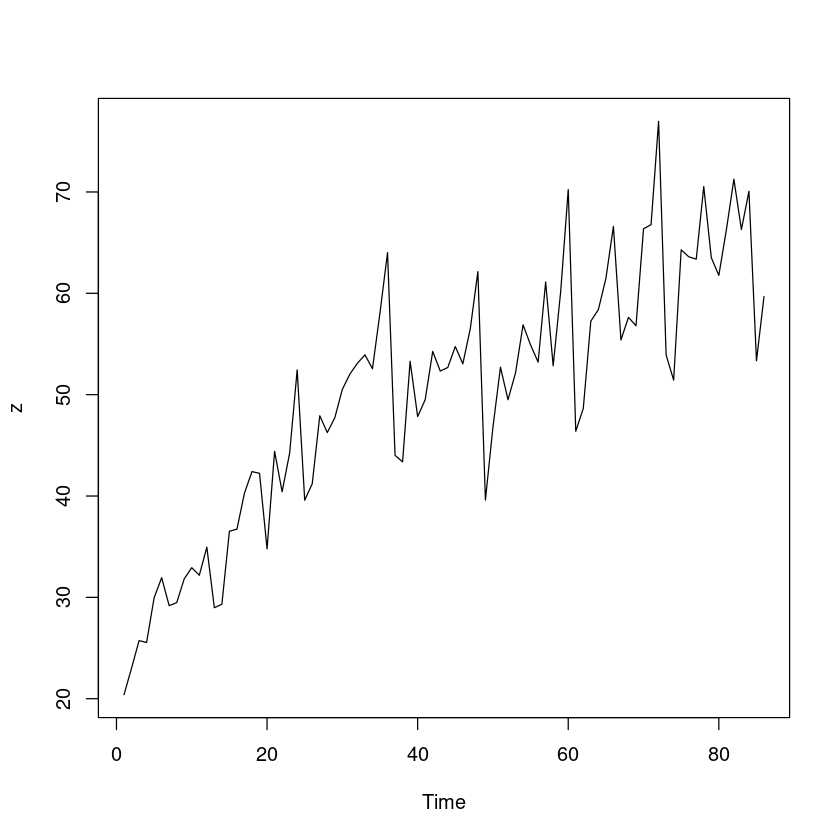

<- scan ("export.txt" )plot.ts (z)

지난 과제에 언급한대로 이 시계열에는 이분산성은 없다고 할 수 있다.

추세와 계절성분이 있으므로 계절주기가 12, 가법형 계절평활법을 사용하는 것이 적합하다.

계절평활을 하기 위해서는 데이터를 ts 객체로 변환해야 한다

<- ts (z, frequency= 12 )

<- HoltWinters (z_ts)

Holt-Winters exponential smoothing with trend and additive seasonal component.

Call:

HoltWinters(x = z_ts)

Smoothing parameters:

alpha: 0.3304767

beta : 0.04369053

gamma: 0.6102758

Coefficients:

[,1]

a 66.9300146

b 0.3670945

s1 -0.9590061

s2 -2.3460160

s3 -1.4388022

s4 4.0020957

s5 -2.8546787

s6 -3.1036803

s7 0.4486017

s8 3.3118493

s9 1.6302355

s10 8.0731659

s11 -11.5480012

s12 -8.8892298

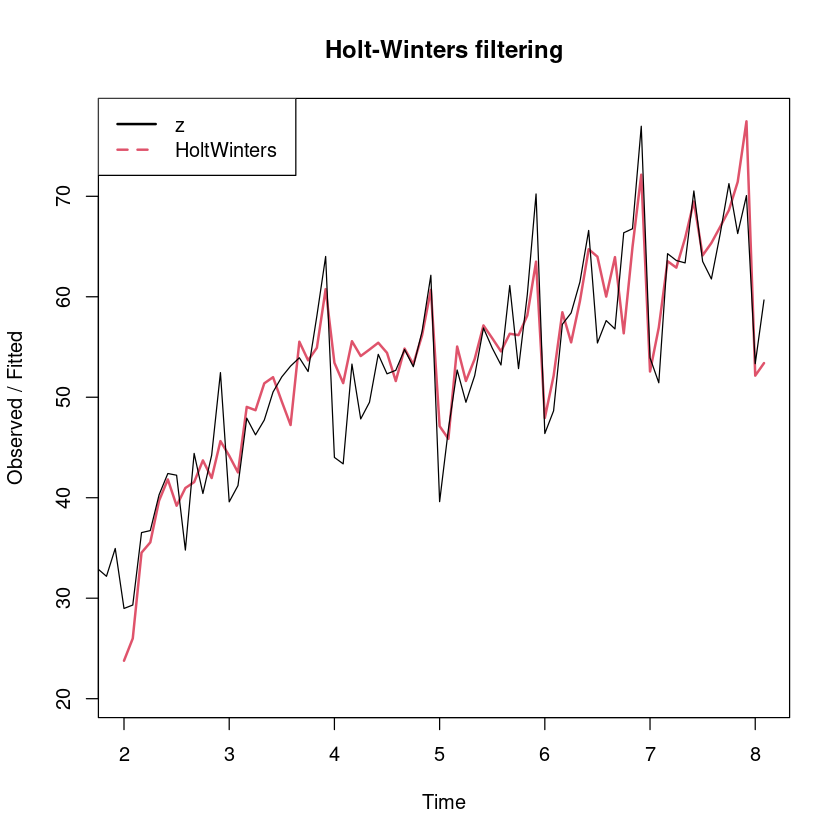

plot (export_smoothing, lwd= 2 , lty= 1 : 2 )legend ("topleft" , legend= c ("z" , "HoltWinters" ), col= 1 : 2 , lty= 1 : 2 , lwd= 2 )

- 예측오차분석

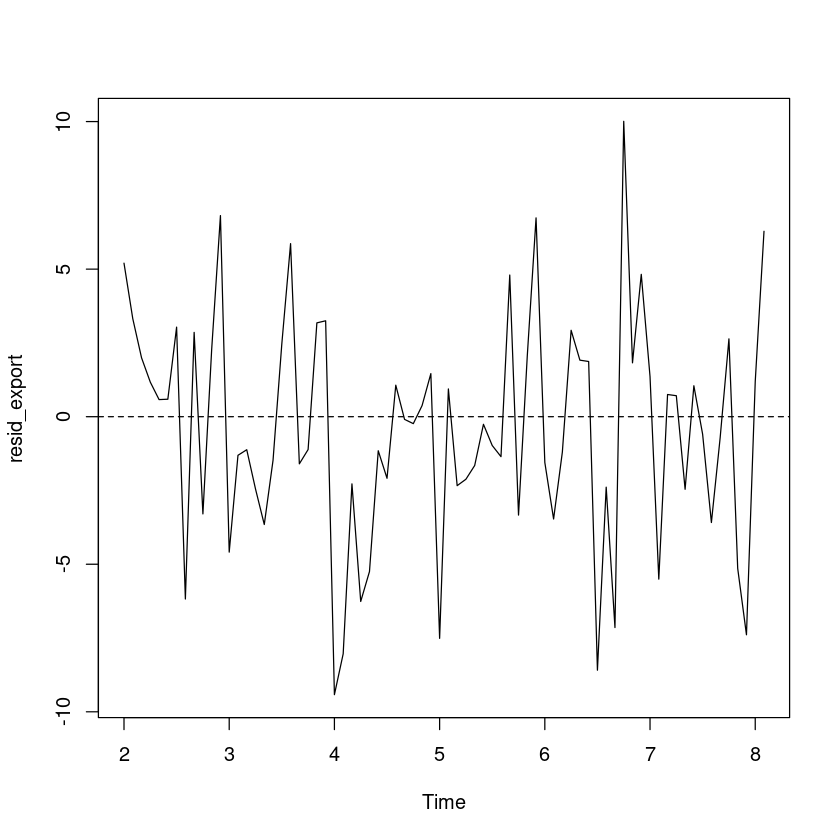

<- resid (export_smoothing)plot.ts (resid_export)abline (h= 0 , lty= 2 )

예측오차의 경우 0을 중심으로 대칭이고, 이분산성은 없어 보인다

One Sample t-test

data: resid_export

t = -0.99304, df = 73, p-value = 0.324

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-1.359825 0.455374

sample estimates:

mean of x

-0.4522256

t-test 결과 예측오차의 평균은 0이라고 할 수 있다.

:: dwtest (lm (resid_export~ 1 ), alternative= "two.sided" )

Durbin-Watson test

data: lm(resid_export ~ 1)

DW = 1.8163, p-value = 0.4267

alternative hypothesis: true autocorrelation is not 0

DW test 결과 예측오차들 간의 자기 상관은 없는 것으로 보인다.

따라서 예측오차는 분석 결과 평활 결과는 적합하다고 할 수 있다.

2장에서 계절추세 모형을 적합한 경우에는 예측오차 간에 자기 상관이 있다는 결과 를 얻었었는데, 평활을 이용한 결과 자기상관이 제거되었다.

- 계절추세모형

<- as.factor (cycle (z_ts))<- 1 : length (z)<- lm (z~ t+ seasonal_I)<- lm (z~ t+ I (t^ 2 )+ seasonal_I)

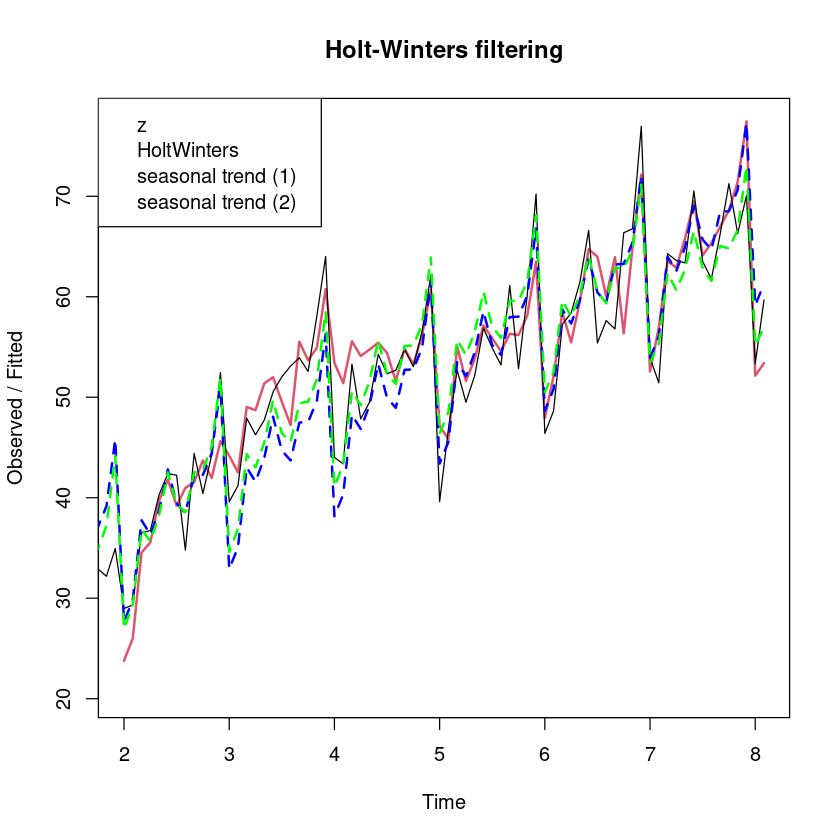

plot (export_smoothing, lwd= 2 , lty= 1 : 2 )lines (ts (fitted (m2), frequency= 12 ), col= 'blue' , lty= 2 , lwd= 2 )lines (ts (fitted (m3), frequency= 12 ), col= 'green' , lty= 2 , lwd= 2 )legend ("topleft" , legend= c ("z" , "HoltWinters" , "seasonal trend (1)" , "seasonal trend (2)" ))

- SSE 비교하기

head (export_smoothing$ fitted) ## 평활값은 12시차 이후값부터 생성됨

A Time Series: 6 × 4

Jan 2

23.77825

28.21682

0.8502812

-5.2888542

Feb 2

25.99728

30.78616

0.9253878

-5.7142708

Mar 2

34.53331

32.80963

0.9733636

0.7503125

Apr 2

35.55911

34.44285

1.0021933

0.1140625

May 2

39.71058

35.83200

1.0190994

2.8594792

Jun 2

41.81786

37.04258

1.0274655

3.7478125

<- sum ((z[- (1 : 12 )]- export_smoothing$ fitted[,1 ])^ 2 ) #또는 <- export_smoothing$ SSE

<- sum (resid (m2)^ 2 )<- sum (resid (m3)^ 2 )

paste0 ("SSE_smomthing = " ,sse_smoothing)paste0 ("SSE_m2 = " , sse_m2)paste0 ("SSE_m3 = " , sse_m3)

'SSE_smomthing = 1135.42182593918'

'SSE_m2 = 1371.05731181319'

'SSE_m3 = 934.603221419272'

모형을 1시차 예측오차에 대한 제곱합으로 비교하면 2차추세모형을 적합한 m3의 SSE값이 가장 작고, 1차선형추세를 사용한 모형의 SSE가 가장 크다.

<- mean ((z[- (1 : 12 )]- export_smoothing$ fitted[,1 ])^ 2 )<- mean (resid (m2)^ 2 )<- mean (resid (m3)^ 2 )paste0 ("MSE_smomthing = " ,mse_smoothing)paste0 ("MSE_m2 = " , mse_m2)paste0 ("MSE_m3 = " , mse_m3)

'MSE_smomthing = 15.3435381883673'

'MSE_m2 = 15.9425268815487'

'MSE_m3 = 10.8674793188287'

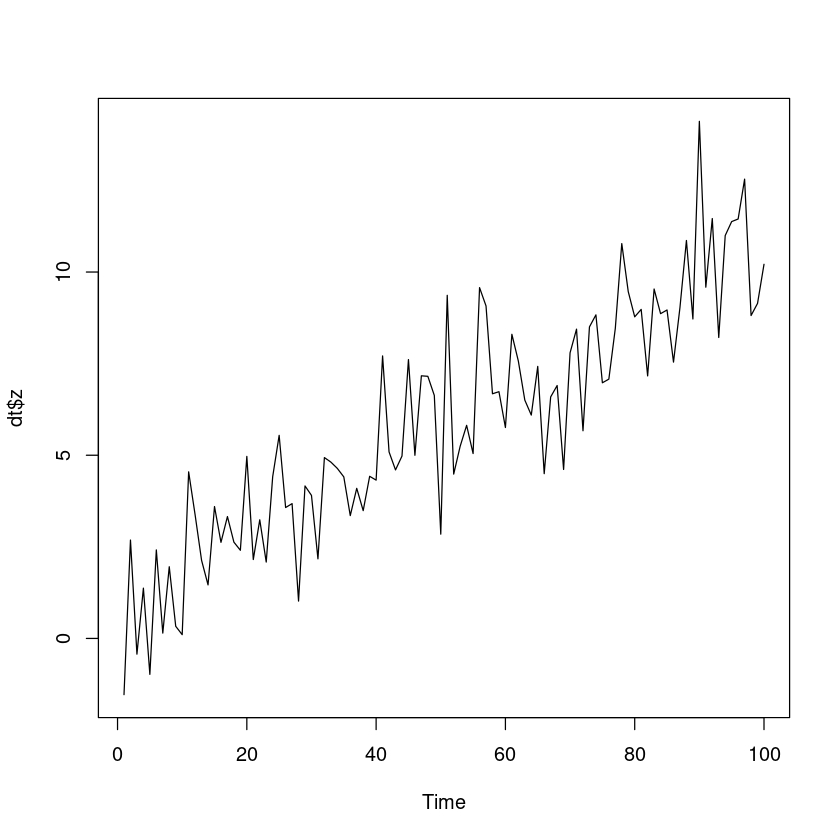

3

(1)

<- read.csv ('data1.csv' )head (dt)

A data.frame: 6 × 3

<int>

<int>

<dbl>

1

1

1

-1.5346871

2

2

2

2.6850469

3

3

3

-0.4288189

4

4

4

1.3724199

5

5

5

-0.9800884

6

6

6

2.4156505

추세가 있음, 계절성분은 없음

선형추세 모형 적합

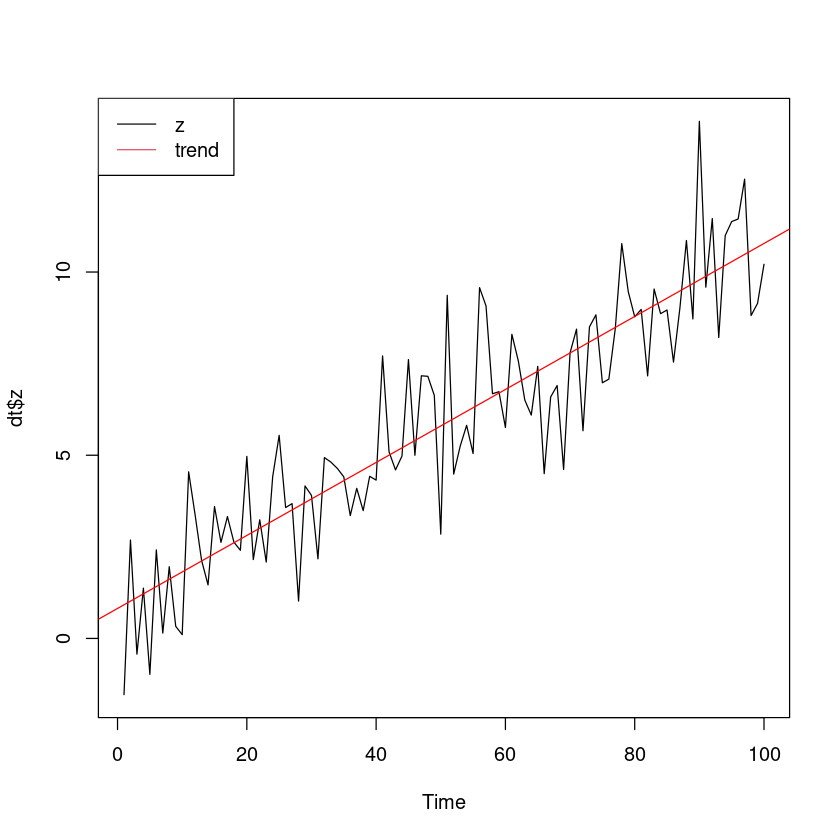

<- lm (z~ t, dt)summary (m_trend)

Call:

lm(formula = z ~ t, data = dt)

Residuals:

Min 1Q Median 3Q Max

-3.0803 -1.0287 0.0169 0.8426 4.3288

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.818932 0.296301 2.764 0.00682 **

t 0.099619 0.005094 19.557 < 2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.47 on 98 degrees of freedom

Multiple R-squared: 0.796, Adjusted R-squared: 0.7939

F-statistic: 382.5 on 1 and 98 DF, p-value: < 2.2e-16

plot.ts (dt$ z)abline (m_trend, col= 'red' )legend ("topleft" , c ("z" , "trend" ), lty= 1 , col= 1 : 2 )

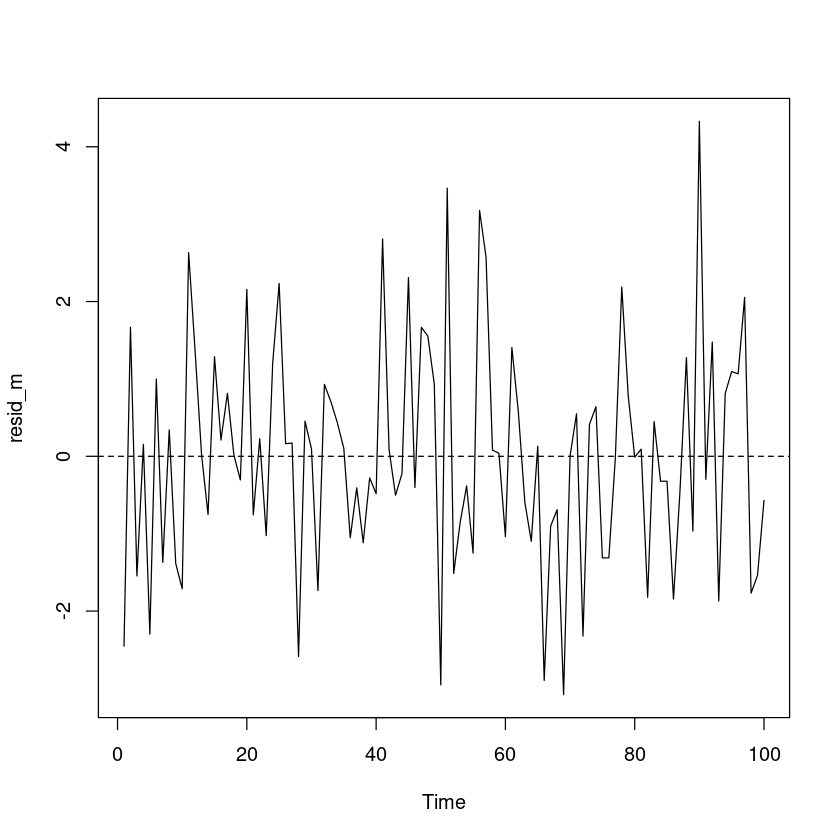

- 잔차분석

<- resid (m_trend)plot.ts (resid_m)abline (h= 0 , lty= 2 )

잔차의 경우 0을 중심으로 대칭이고, 이분산성은 없어 보인다.

One Sample t-test

data: resid_m

t = -5.2362e-16, df = 99, p-value = 1

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-0.2902834 0.2902834

sample estimates:

mean of x

-7.660376e-17

t-test 결과 예측오차의 평균은 0이라고 할 수 있다

Durbin-Watson test

data: m_trend

DW = 2.2164, p-value = 0.8389

alternative hypothesis: true autocorrelation is greater than 0

(2)

<- data.frame (t= 100 + (1 : 10 ))<- predict (m_trend, new_dt)

1 10.8804416292757 2 10.9800605357706 3 11.0796794422655 4 11.1792983487603 5 11.2789172552552 6 11.3785361617501 7 11.4781550682449 8 11.5777739747398 9 11.6773928812347 10 11.7770117877295

(3)

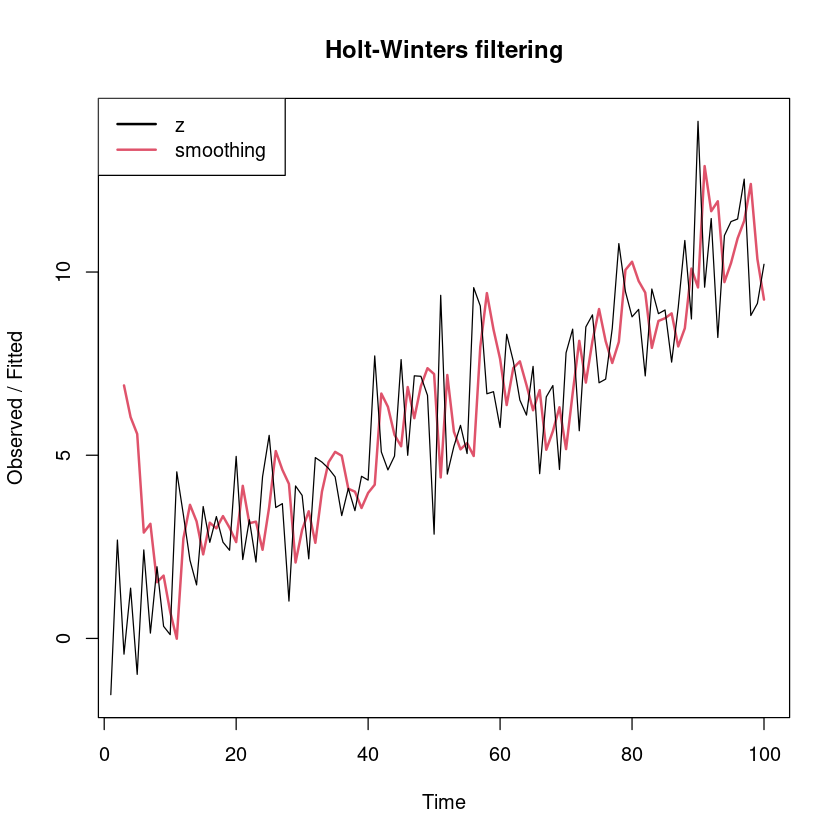

<- HoltWinters (dt$ z, gamma= FALSE )

Holt-Winters exponential smoothing with trend and without seasonal component.

Call:

HoltWinters(x = dt$z, gamma = FALSE)

Smoothing parameters:

alpha: 0.496601

beta : 0.396225

gamma: FALSE

Coefficients:

[,1]

a 9.7266353

b -0.3150449

plot (m_smoothing, lwd= 2 )legend ("topleft" , legend= c ("z" ,"smoothing" ), lty= 1 , lwd= 2 , col= 1 : 2 )

- 예측오차 분석

<- dt$ z[- (1 : 2 )] - m_smoothing$ fitted[,1 ] #또는 <- resid (m_smoothing) #같은 방법임

plot.ts (resid_smoothing)abline (h= 0 , lty= 2 )

예측오차의 경우 0을 중심으로 대칭이고, 이분산성은 없어 보인다.

One Sample t-test

data: resid_smoothing

t = -1.0711, df = 97, p-value = 0.2868

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-0.6709125 0.2005740

sample estimates:

mean of x

-0.2351693

t-test 결과 예측오차의 평균은 0이라고 할 수 있다.

:: dwtest (lm (resid_smoothing~ 1 ), alternative= "two.sided" )

Durbin-Watson test

data: lm(resid_smoothing ~ 1)

DW = 1.9664, p-value = 0.8675

alternative hypothesis: true autocorrelation is not 0

(4)

<- predict (m_smoothing, n.ahead= 10 , prediction.interval = T, level= 0.95 )

A Time Series: 10 × 3

101

9.411590

13.67142

5.1517644

102

9.096545

14.28017

3.9129175

103

8.781500

15.20395

2.3590541

104

8.466456

16.38382

0.5490889

105

8.151411

17.77356

-1.4707380

106

7.836366

19.34098

-3.6682458

107

7.521321

21.06388

-6.0212357

108

7.206276

22.92649

-8.5139377

109

6.891231

24.91716

-11.1346959

110

6.576186

27.02692

-13.8745530

:: holt (dt$ z, alpha = m_smoothing$ alpha, beta= m_smoothing$ beta, h= 10 )#, initial)

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

101 8.862685 6.0523463 11.67302 4.564643 13.16073

102 8.360702 4.5932352 12.12817 2.598859 14.12254

103 7.858719 2.6320999 13.08534 -0.134705 15.85214

104 7.356735 0.3034311 14.41004 -3.430363 18.14383

105 6.854752 -2.3086731 16.01818 -7.159497 20.86900

106 6.352769 -5.1561498 17.86169 -11.248603 23.95414

107 5.850786 -8.2094249 19.91100 -15.652451 27.35402

108 5.348803 -11.4485541 22.14616 -20.340538 31.03814

109 4.846819 -14.8590196 24.55266 -25.290661 34.98430

110 4.344836 -18.4296256 27.11930 -30.485697 39.17537

잘려서 뒤에가 뭐라고 써있는지를 모르겠음. initial값에 뭘 지정하는 것 같은데 똑같은 값이 안나온다

(5)

<- read.csv ("data1_new.csv" )

A data.frame: 10 × 3

<int>

<int>

<dbl>

1

101

11.577471

2

102

13.171004

3

103

12.730258

4

104

12.242375

5

105

10.877077

6

106

13.297355

7

107

14.632224

8

108

15.049088

9

109

9.671734

10

110

12.216420

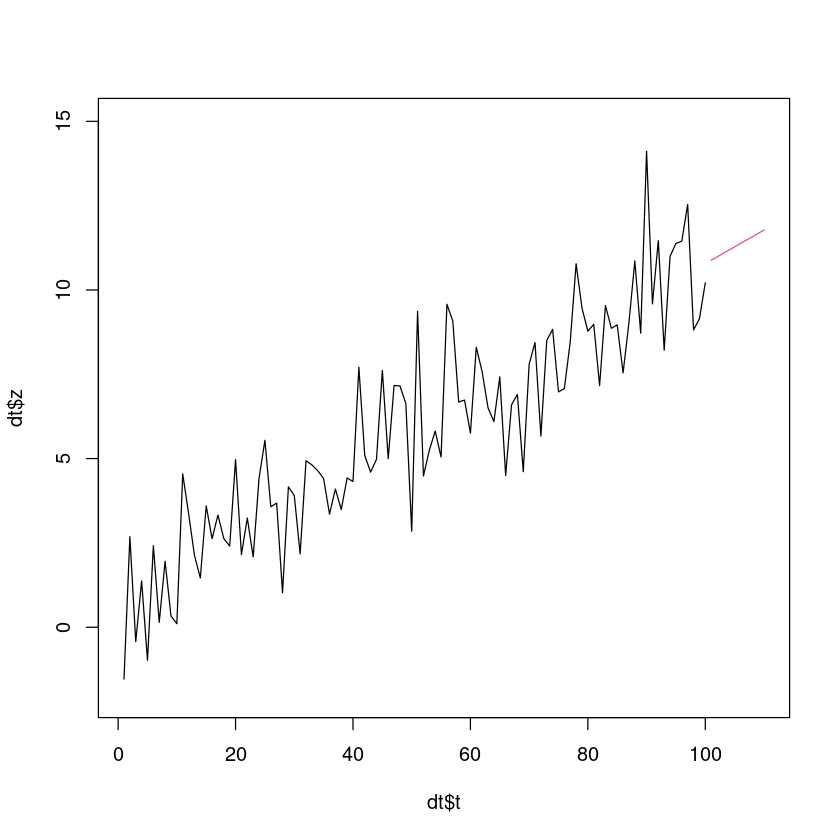

plot (dt$ t,dt$ z, xlim= c (1 ,110 ), ylim= c (- 2 , 15 ), type= 'l' )lines (101 : 110 , pred_trend, col= 2 )lines (101 : 110 , pred_smoothing, col= 3 )

ERROR: Error in xy.coords(x, y): 'x' and 'y' lengths differ

MSE, MAPE, MAE 값을 이용하여 비교할 수 있다.

\(MSE = \dfrac{1}{m} \sum_{i=1}^n \hat e_{n-1+t}(1)^2\)

\(MAPE = \dfrac{100}{n} \sum_{i=1}^n \left| \dfrac{\hat e_{n-1+t}(1)}{Z_{n+t}} \right|\)

\(MAE = \dfrac{1}{m} \sum_{i=1}^m \left| \hat e_{n-1+t}(1) \right|\)

<- real_new_dt$ z - pred_trend<- real_new_dt$ z - pred_smoothing

MSE_trend = mean (e_trend^ 2 ))MSE_smoothing = mean (e_smoothing^ 2 ))MAPE_trend = 100 * sum (abs (e_trend/ real_new_dt$ z)) / 10 )MAPE_smoothing = 100 * sum (abs (e_smoothing/ real_new_dt$ z)) / 10 )MAE_trend = mean (abs (e_trend)))MAE_smoothing = mean (abs (e_smoothing)))

3.91978903404576

127.173436899506

13.1385437579375

218.735568237967

1.69927387507187

9.02750167882282

교수님 풀이랑 smoothing 의 값이 좀 다르다.

4

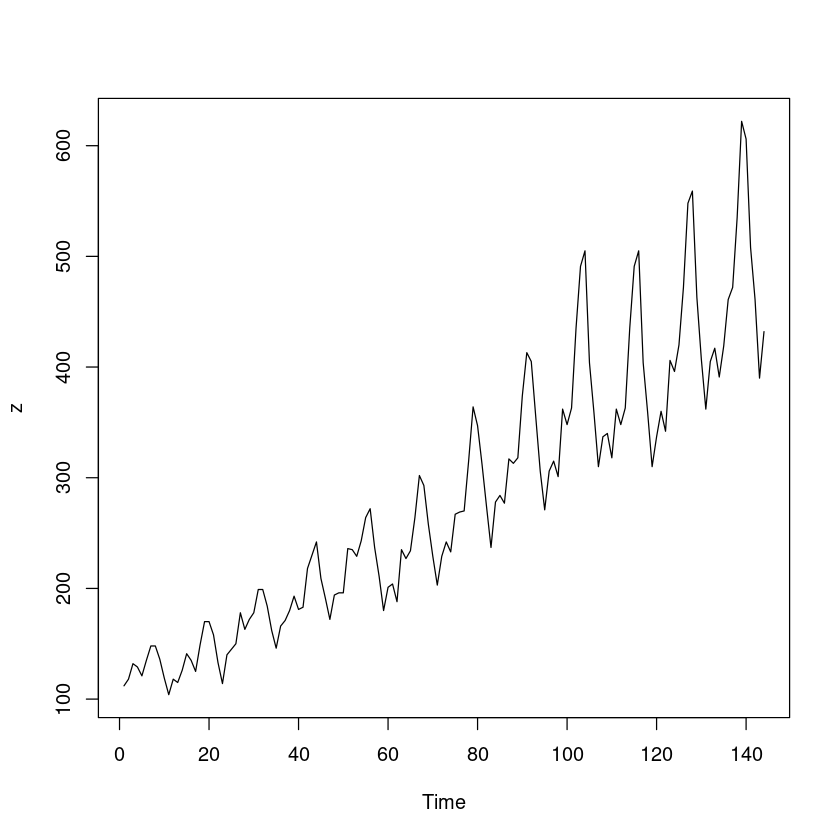

<- scan ('export.txt' )plot.ts (z)

(1)

위에서 2차선형추세 모형이 더 적절했다고 했으므로, 2차 추세 모형을 적합한다.

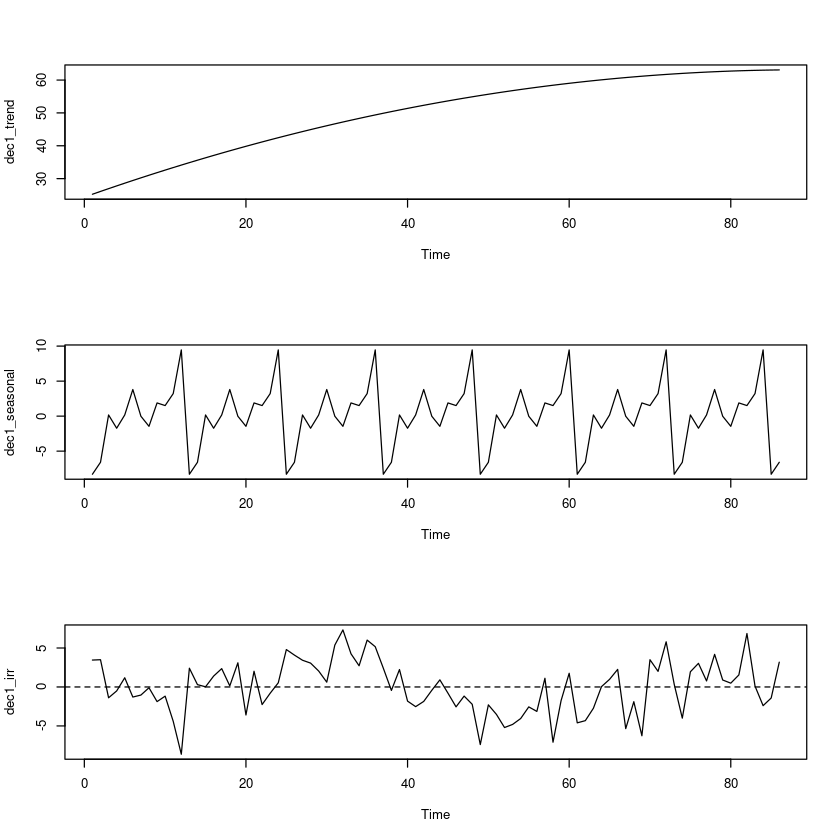

<- ts (z, frequency= 12 )<- as.factor (cycle (z_ts))<- 1 : length (z)

<- fitted (lm (z~ t+ I (t^ 2 ))) ## 추세성분

= z- dec1_trend<- fitted (lm (adjtrend ~ 0 + seasonal_I)) ## 계절성분

= z- dec1_trend- dec1_seasonal ## 불규칙 성분

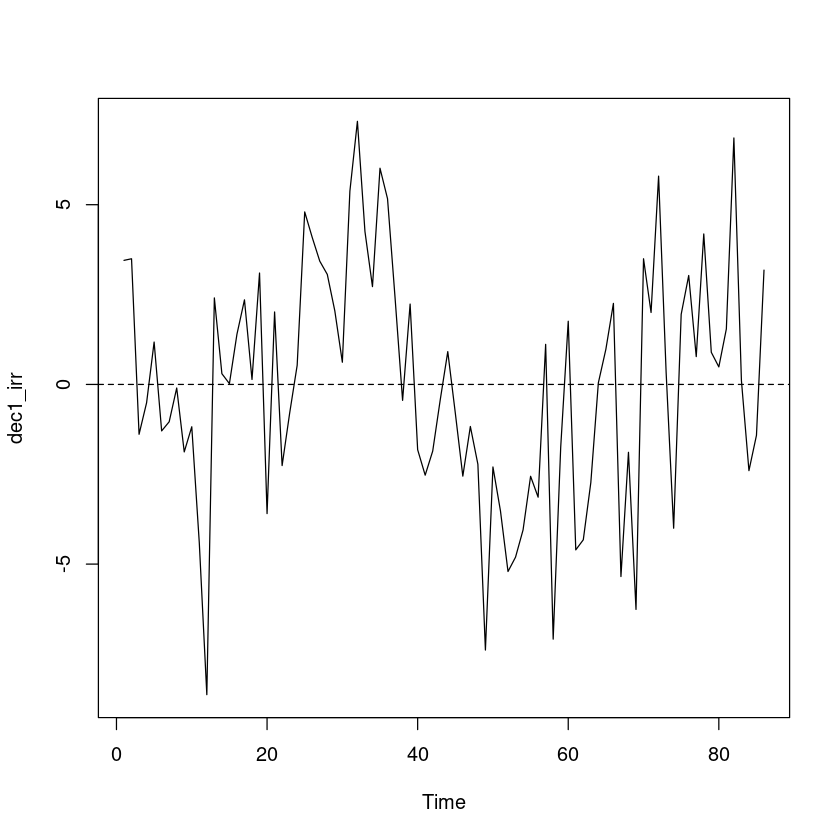

par (mfrow= c (3 ,1 ))plot.ts (dec1_trend)plot.ts (dec1_seasonal)plot.ts (dec1_irr)abline (h= 0 , lty= 2 )= c (1 ,1 )

(2)

plot.ts (dec1_irr)abline (h= 0 , lty= 2 )

예측오차의 경우 0을 중심으로 대칭이고, 이분산성은 보이지 않는다.

One Sample t-test

data: dec1_irr

t = 2.2831e-16, df = 85, p-value = 1

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-0.7179805 0.7179805

sample estimates:

mean of x

8.244475e-17

t-test 결과 예측오차의 평균은 0이라고 할 수 있다.

:: dwtest (lm (dec1_irr~ 1 ), alternative= "two.sided" )

Durbin-Watson test

data: lm(dec1_irr ~ 1)

DW = 1.1429, p-value = 2.78e-05

alternative hypothesis: true autocorrelation is not 0

(3)

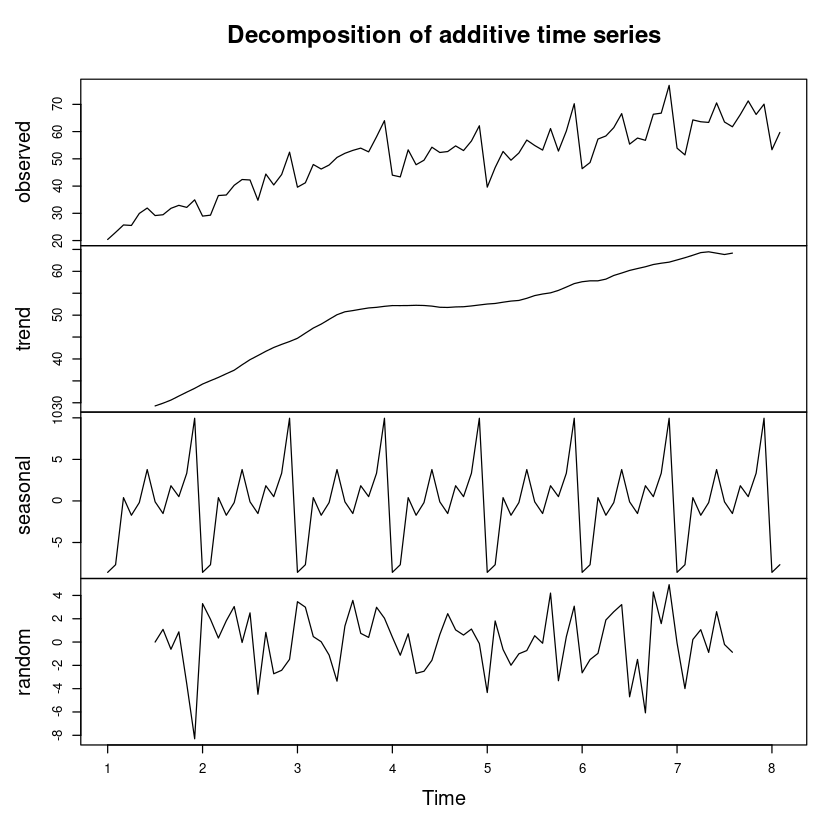

<- decompose (z_ts, 'additive' )plot (dec_fit)

(4)

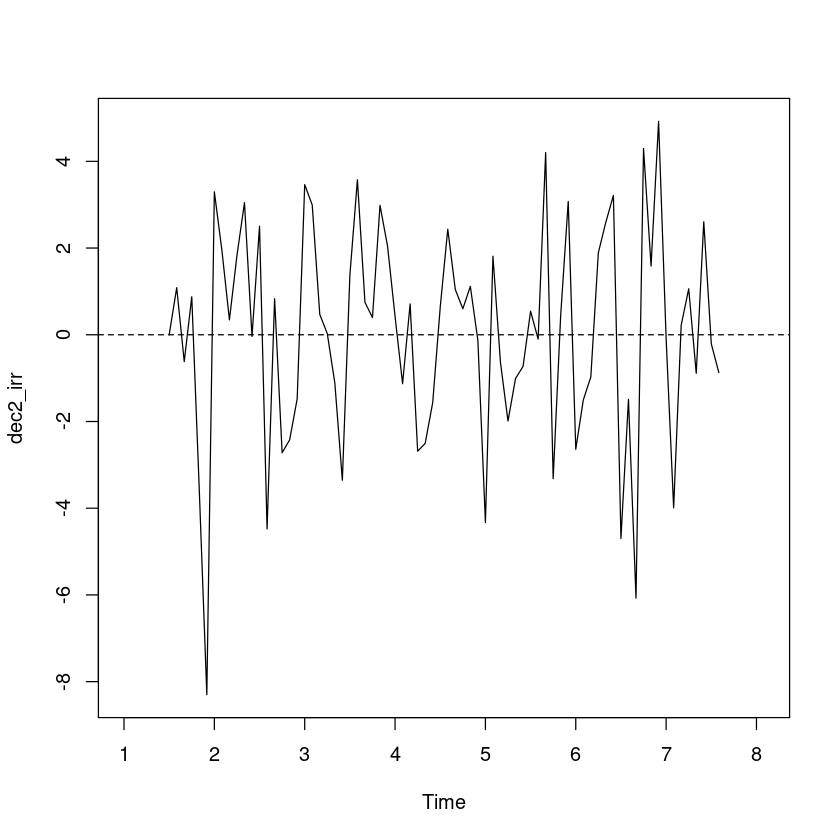

<- dec_fit$ randomplot.ts (dec2_irr)abline (h= 0 , lty= 2 )

예측오차의 경우 0을 중심으로 대칭이고, 이분산성은 없어 보인다.

One Sample t-test

data: dec2_irr

t = 0.074013, df = 73, p-value = 0.9412

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-0.5674456 0.6112171

sample estimates:

mean of x

0.02188575

t-test 결과 예측오차의 평균은 0이라고 할 수 있다

:: dwtest (lm (dec2_irr~ 1 ), alternative= "two.sided" )

Durbin-Watson test

data: lm(dec2_irr ~ 1)

DW = 1.9469, p-value = 0.8188

alternative hypothesis: true autocorrelation is not 0

DW test 결과 예측오차들 간의 자기 상관은 없는 것으로 보인다.

따라서 예측오차는 분석 결과 평활 결과는 적절하다고 할 수 있다.

추세를 이용한 분해법에서 예측 오차는 상관관계가 있었지만, 평활법을 사용하면서 예측오차들의 상관관계를 제거할 수 있었다.

(5)

= sum (dec1_irr^ 2 )= sum (dec2_irr^ 2 , na.rm= T)paste0 ("SSE_1 = " , sse_1)paste0 ("SSE_2 = " , sse_2)

'SSE_1 = 953.219486362055'

'SSE_2 = 472.381499188028'

SSE 값을 비교하였을 때, 평활에 의한 분해법의 값이 더 작다.

= mean (dec1_irr^ 2 )= mean (dec2_irr^ 2 , na.rm= T)paste0 ("MSE_1 = " , mse_1)paste0 ("MSE_2 = " , mse_2)

'MSE_1 = 11.0839475158378'

'MSE_2 = 6.38353377281119'

5

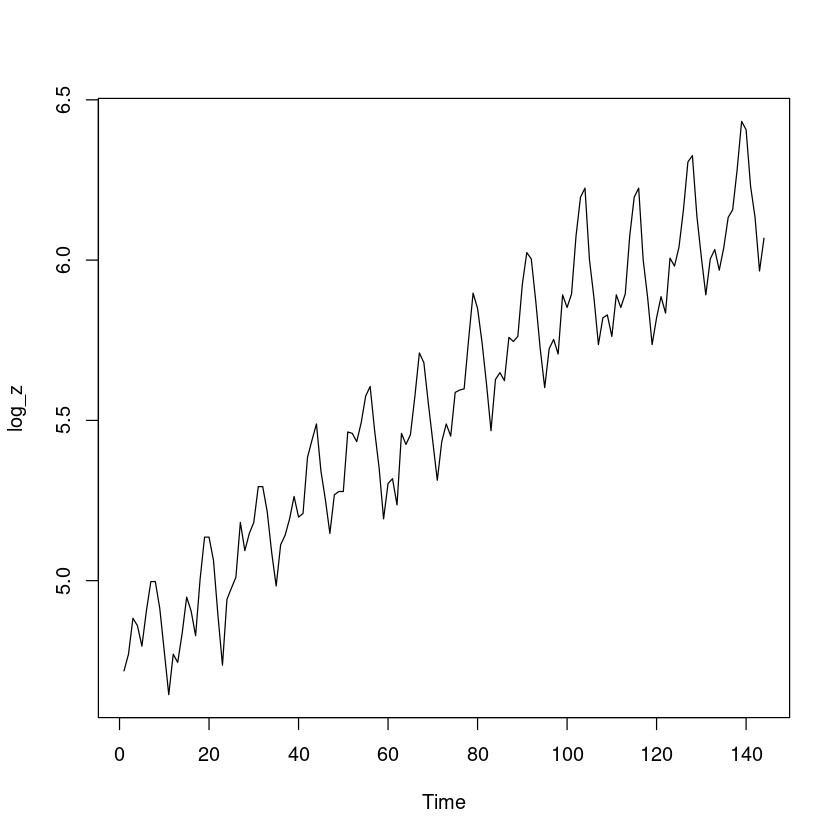

<- scan ('usapass.txt' )plot.ts (z)

(1)

<- log (z)plot.ts (log_z)

(2)

지수함수를 사용한 계절형 추세모형을 적합한다.

<- ts (z, frequency= 12 )= log (z_ts)<- as.factor (cycle (log_z_ts))<- 1 : length (z)<- lm (log_z_ts~ 0 + t+ seasonal_I)summary (m_trend)

Call:

lm(formula = log_z_ts ~ 0 + t + seasonal_I)

Residuals:

Min 1Q Median 3Q Max

-0.159814 -0.044426 0.000623 0.045572 0.151846

Coefficients:

Estimate Std. Error t value Pr(>|t|)

t 0.0100999 0.0001252 80.67 <2e-16 ***

seasonal_I1 4.7246982 0.0198289 238.27 <2e-16 ***

seasonal_I2 4.7026123 0.0198822 236.52 <2e-16 ***

seasonal_I3 4.8342011 0.0199361 242.49 <2e-16 ***

seasonal_I4 4.8015084 0.0199907 240.19 <2e-16 ***

seasonal_I5 4.8009618 0.0200459 239.50 <2e-16 ***

seasonal_I6 4.9237482 0.0201017 244.94 <2e-16 ***

seasonal_I7 5.0296649 0.0201582 249.51 <2e-16 ***

seasonal_I8 5.0223242 0.0202153 248.44 <2e-16 ***

seasonal_I9 4.8708171 0.0202729 240.26 <2e-16 ***

seasonal_I10 4.7357833 0.0203312 232.93 <2e-16 ***

seasonal_I11 4.5905564 0.0203901 225.14 <2e-16 ***

seasonal_I12 4.7032829 0.0204496 229.99 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.06224 on 131 degrees of freedom

Multiple R-squared: 0.9999, Adjusted R-squared: 0.9999

F-statistic: 8.844e+04 on 13 and 131 DF, p-value: < 2.2e-16

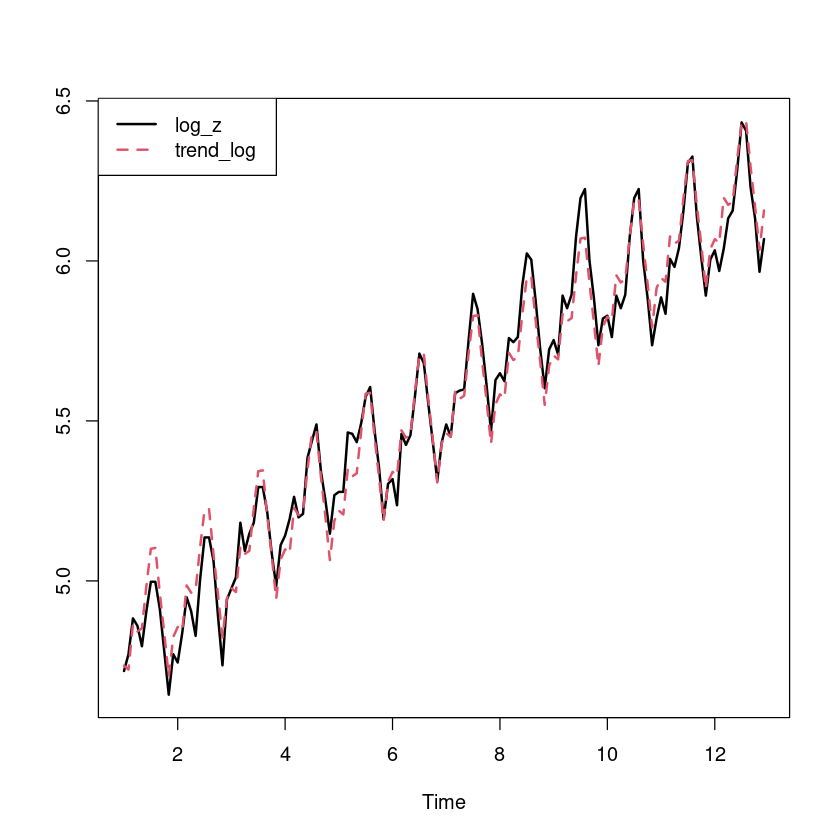

\(\hat Z_t = 0.01t + 4.72I_1 + 4.70I_2 + \dots + 4.70I_{12}\)

ts.plot (log_z_ts, ts (fitted (m_trend), frequency= 12 ), col= 1 : 2 , lty= 1 : 2 , lwd= 2 )legend ("topleft" , c ("log_z" , "trend_log" ), col= 1 : 2 , lty= 1 : 2 , lwd= 2 )

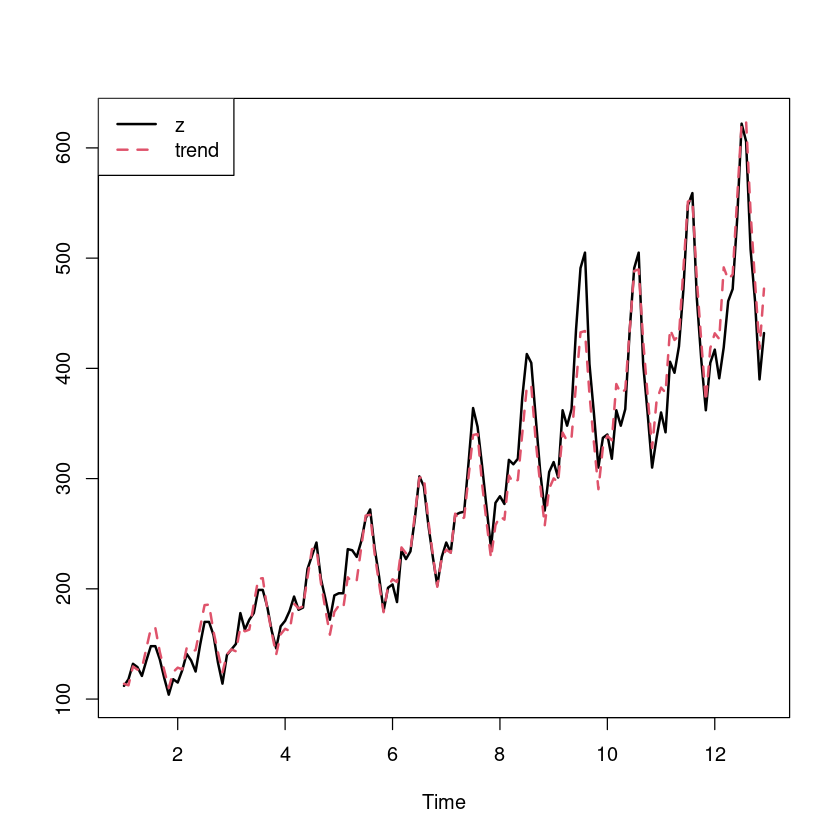

ts.plot (z_ts, ts (exp (fitted (m_trend)), frequency= 12 ), col= 1 : 2 , lty= 1 : 2 , lwd= 2 )legend ("topleft" , c ("z" , "trend" ), col= 1 : 2 , lty= 1 : 2 , lwd= 2 )

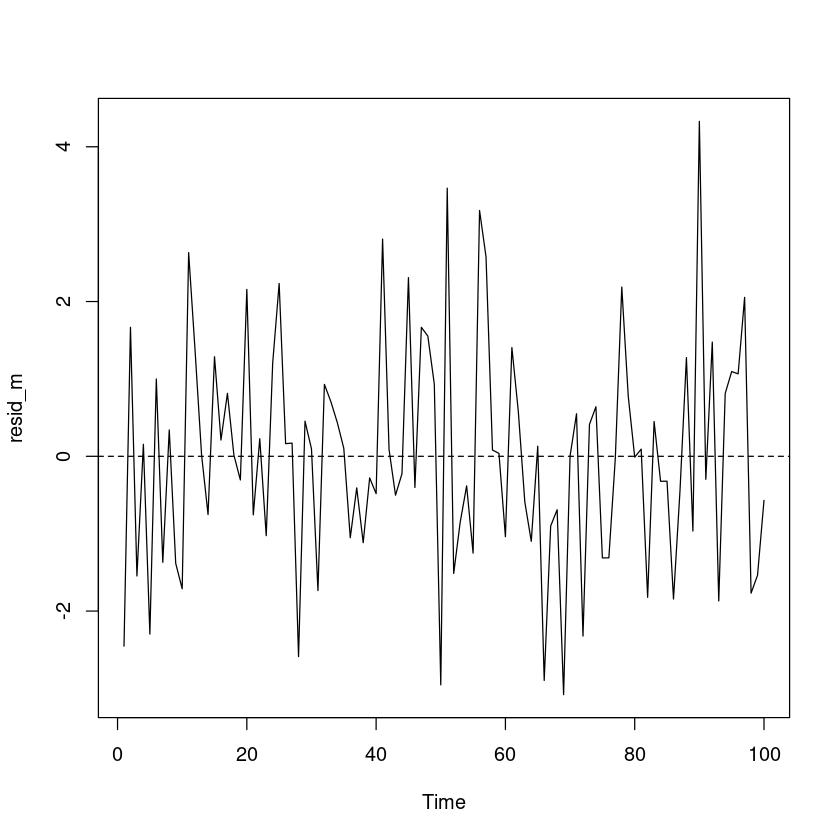

- 잔차분석

<- resid (m_trend)plot.ts (resid_m)abline (h= 0 , lty= 2 )

잔차의 경우 0을 중심으로 대칭이고, 이분산성은 없어 보인다

One Sample t-test

data: resid_m

t = -5.2362e-16, df = 99, p-value = 1

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-0.2902834 0.2902834

sample estimates:

mean of x

-7.660376e-17

t-test 결과 예측오차의 평균은 0이라고 할 수 있다.

:: dwtest (m_trend, alternative= "two.sided" )

Durbin-Watson test

data: m_trend

DW = 0.40831, p-value < 2.2e-16

alternative hypothesis: true autocorrelation is not 0

(3)

- 로그변환한 데이터에 대한 가법 모형

<- HoltWinters (log_z_ts)

Holt-Winters exponential smoothing with trend and additive seasonal component.

Call:

HoltWinters(x = log_z_ts)

Smoothing parameters:

alpha: 0.3447498

beta : 0.003585913

gamma: 0.879488

Coefficients:

[,1]

a 6.165298459

b 0.008744433

s1 -0.073696849

s2 -0.142822821

s3 -0.039964334

s4 0.015968620

s5 0.033673237

s6 0.157016140

s7 0.300626468

s8 0.285698068

s9 0.098491289

s10 -0.021898771

s11 -0.190036243

s12 -0.096734648

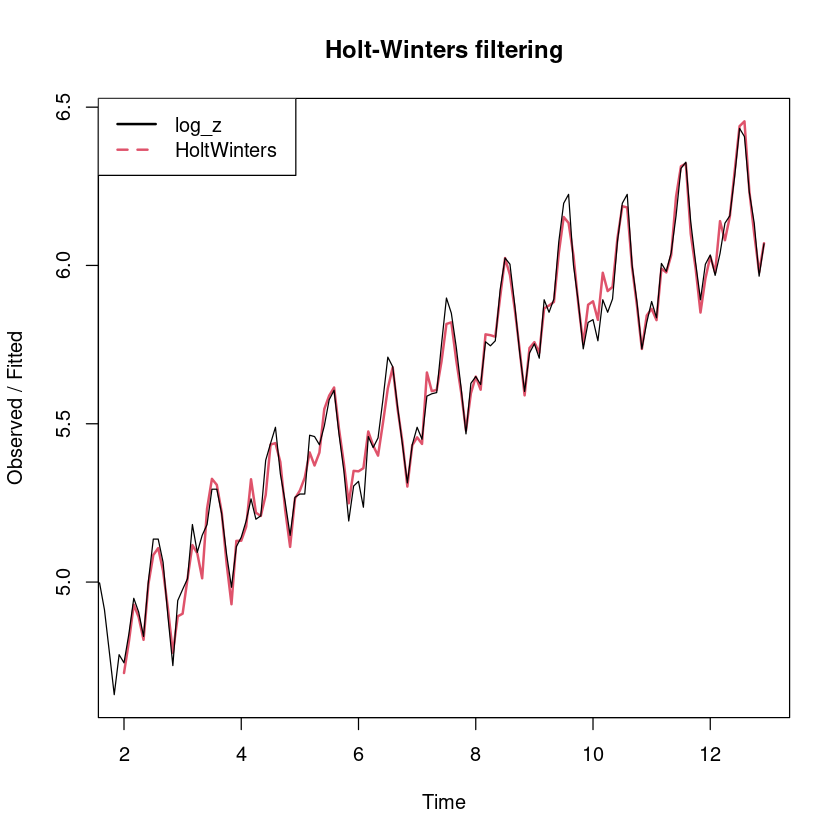

plot (m_smoothing, lwd= 2 , lty= 1 : 2 )legend ("topleft" , legend= c ("log_z" , "HoltWinters" ), col= 1 : 2 , lty= 1 : 2 , lwd= 2 )

- 잔차분석

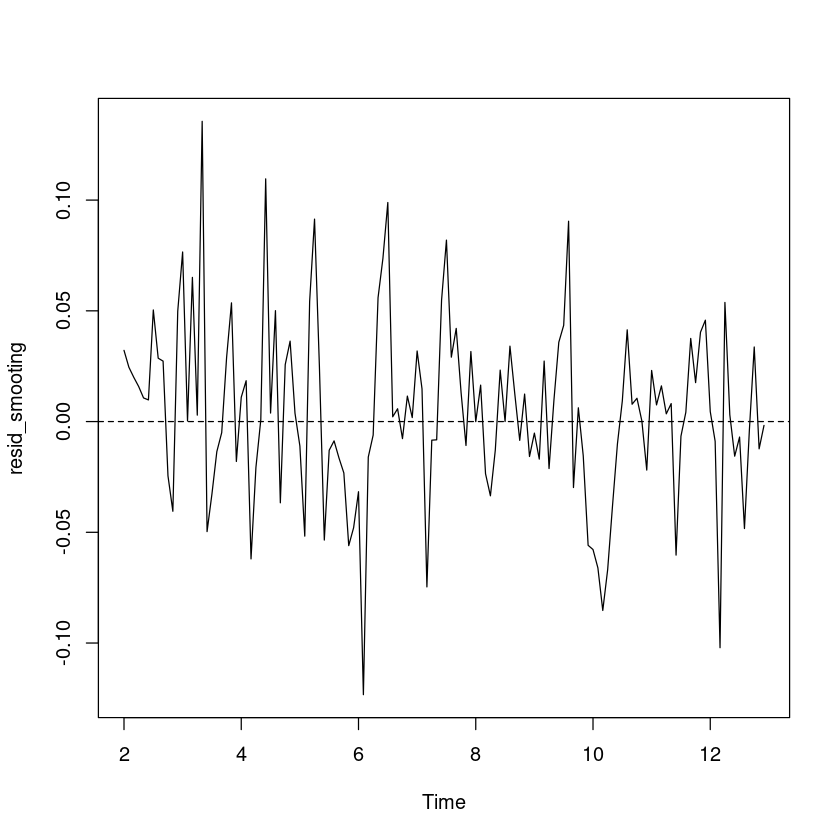

<- resid (m_smoothing)plot.ts (resid_smooting)abline (h= 0 , lty= 2 )

예측오차의 경우 0을 중심으로 대칭이고, 이분산성은 없어 보인다.

One Sample t-test

data: resid_smooting

t = 1.2026, df = 131, p-value = 0.2313

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-0.002766709 0.011346227

sample estimates:

mean of x

0.004289759

t-test 결과 예측오차의 평균은 0이라고 할 수 있다.

:: dwtest (lm (resid_smooting~ 1 ), alternative= "two.sided" )

Durbin-Watson test

data: lm(resid_smooting ~ 1)

DW = 1.4549, p-value = 0.001604

alternative hypothesis: true autocorrelation is not 0

DW test 결과 예측오차들 간의 자기 상관이 있는 것으로 보인다.

하지만, 추세모형을 적합하였을 때 얻어진 잔차에 비해 유의확률값이 크다.

예측오차는 분석 결과 추세모형 적합 결과보다는 평활 결과가 더 적절하다고 할 수 있다.

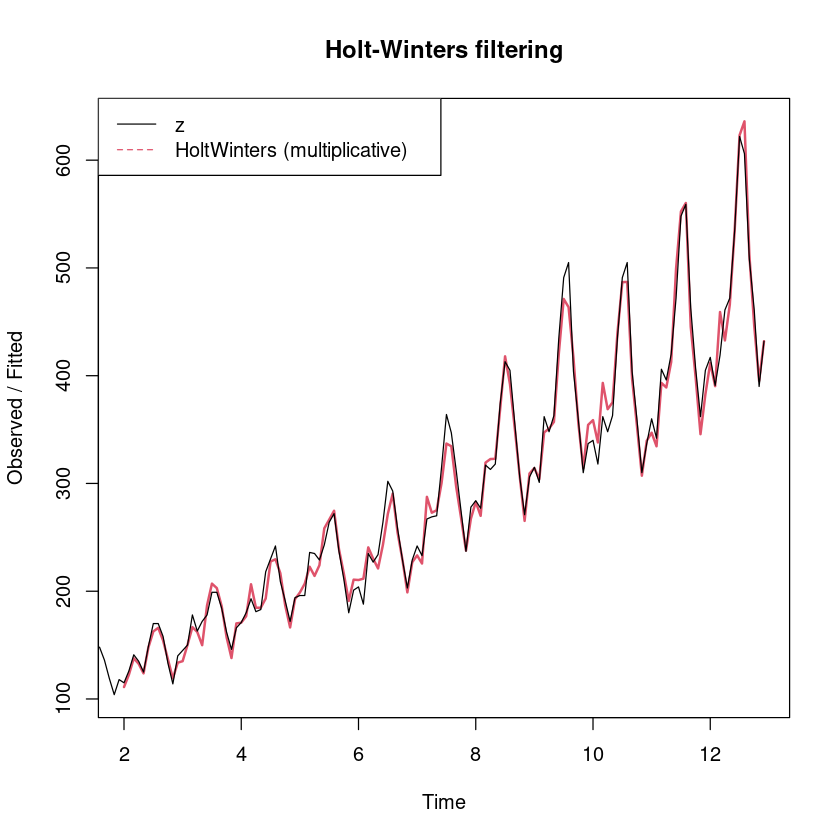

- 원 데이터에 대한 승법모형 적용

<- HoltWinters (z_ts, seasonal = "multiplicative" )

Holt-Winters exponential smoothing with trend and multiplicative seasonal component.

Call:

HoltWinters(x = z_ts, seasonal = "multiplicative")

Smoothing parameters:

alpha: 0.3204565

beta : 0.02388265

gamma: 1

Coefficients:

[,1]

a 464.9721064

b 2.7859138

s1 0.9464640

s2 0.8810274

s3 0.9648716

s4 1.0334898

s5 1.0470250

s6 1.1793118

s7 1.3631491

s8 1.3399425

s9 1.1195987

s10 0.9993794

s11 0.8438225

s12 0.9290880

plot (m_smoothing_multi, lwd= 2 , lty= 1 : 2 )legend ("topleft" , legend= c ("z" , "HoltWinters (multiplicative)" ), col= 1 : 2 , lty= 1 : 2 )

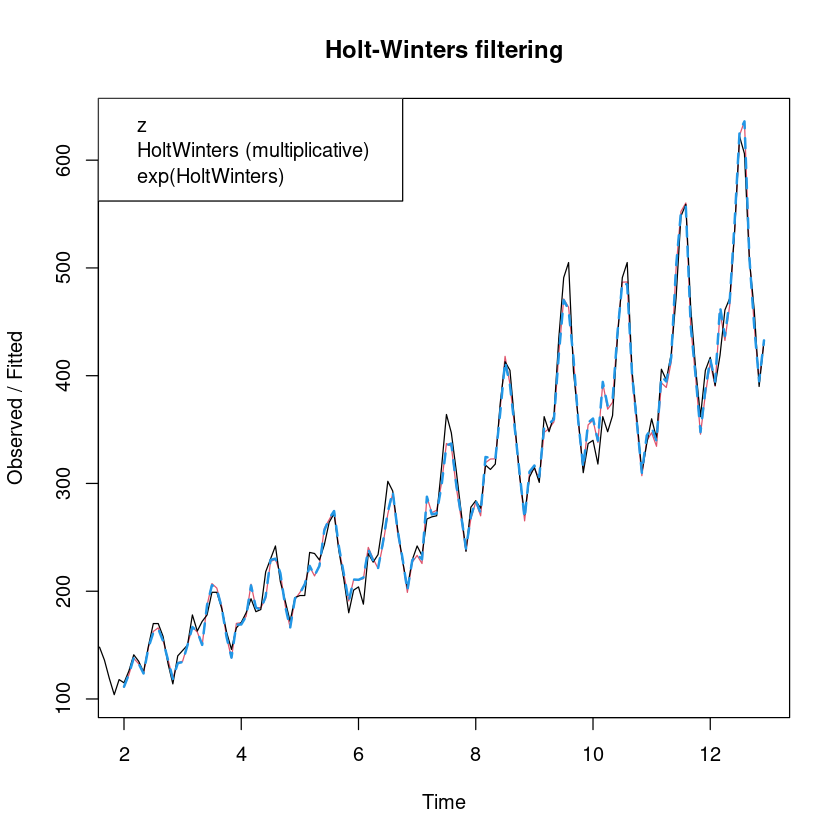

plot (m_smoothing_multi, lwd= 1 : 2 , lty= 1 : 2 )lines (exp (m_smoothing$ fitted[,1 ]), col= 4 , lty= 2 , lwd= 2 )legend ("topleft" , legend= c ("z" , "HoltWinters (multiplicative)" , "exp(HoltWinters)" ))

- 승법모형에 대한 잔차분석

<- resid (m_smoothing_multi)plot.ts (resid_smooting_multi)abline (h= 0 , lty= 2 )

예측오차의 경우 0을 중심으로 대칭이고, 이분산성은 없어 보인다.

t.test (resid_smooting_multi)

One Sample t-test

data: resid_smooting_multi

t = 1.5746, df = 131, p-value = 0.1178

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-0.4315512 3.7983414

sample estimates:

mean of x

1.683395

t-test 결과 예측오차의 평균은 0이라고 할 수 있다.

DW test 결과 예측오차들 간의 자기 상관이 있는 것으로 보인다.

하지만, 추세모형을 적합하였을 때 얻어진 잔차에 비해 유의확률값이 크지만, 가법 모형을 사용한 평활법에 비하면 조금 크다.

차이가 크지 않지만, 가법 모형이 더 적절하다고 할 수 있다. 따라서 가법 모형 사용.

(4)

로그변환한 데이터에 대한 가법모형을 사용하거나, 원래 데이터에 대한 승법 모형 적합 가능

decompose 함수 사용

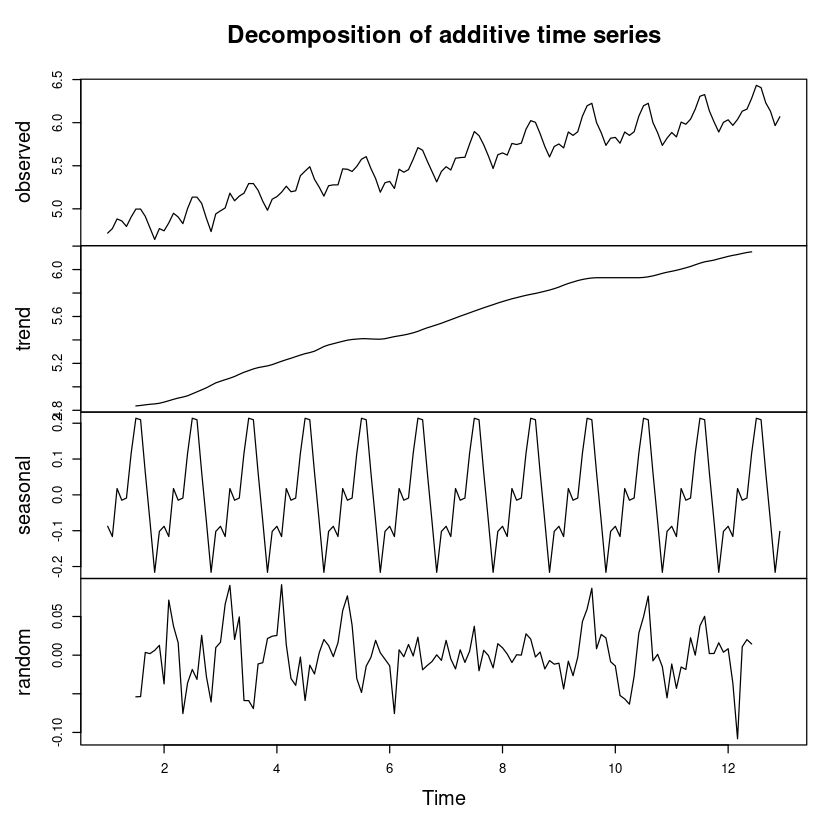

<- decompose (log_z_ts, 'additive' )plot (m_decompose_add)

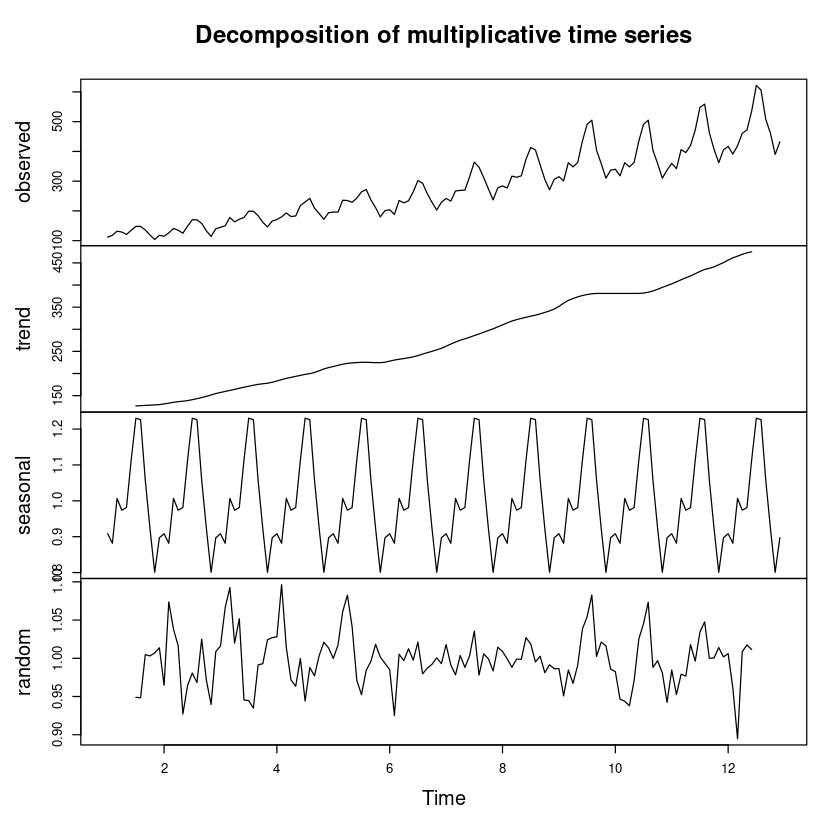

<- decompose (z_ts, 'multiplicative' )plot (m_decompose_multi)

<- m_decompose_add$ trend + m_decompose_add$ seasonal #가법모형은 더 <- m_decompose_multi$ trend * m_decompose_multi$ seasonal #승법모

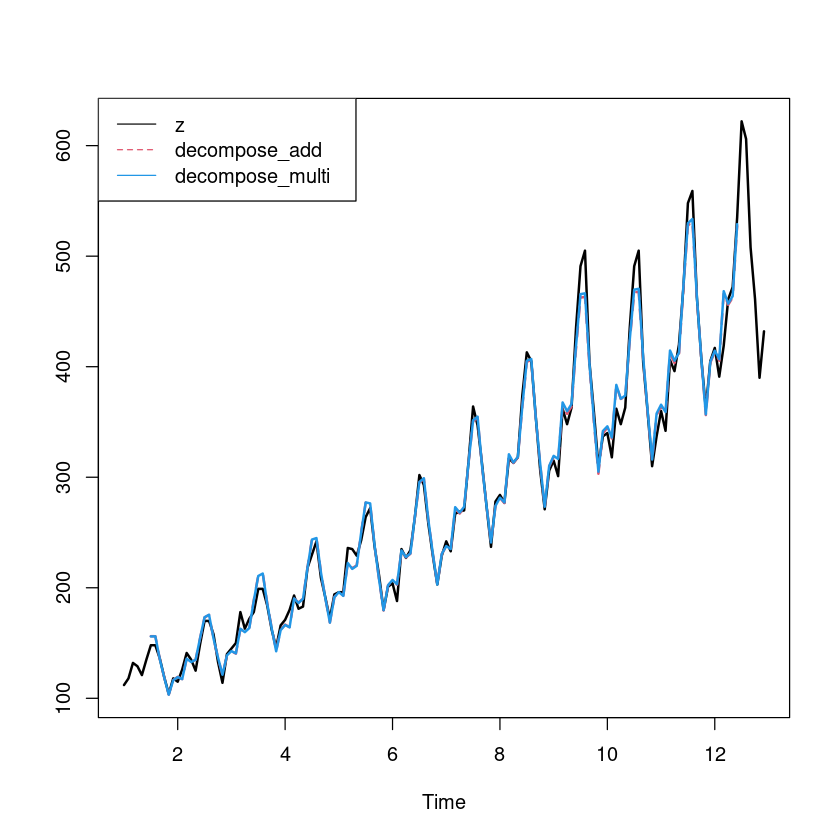

ts.plot (z_ts, exp (fitted_dec_add), fitted_dec_multi, col= c (1 ,2 ,4 ), lwd= 2 , lty= 1 : 2 )legend ("topleft" , c ("z" ,"decompose_add" , "decompose_multi" ), col= c (1 ,2 ,4 ), lty= 1 : 2 )

가법모형과 승법 모형은 차이가 거의 없어 보임

- 잔차분석을 하라는 문제는 없었지만 한 번 해보겠음.

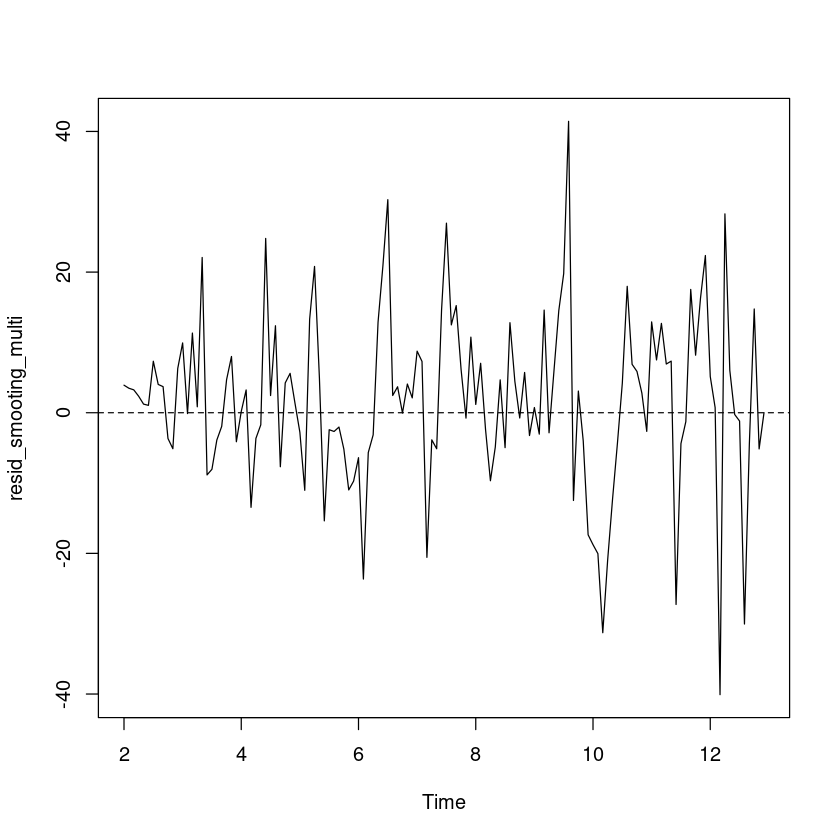

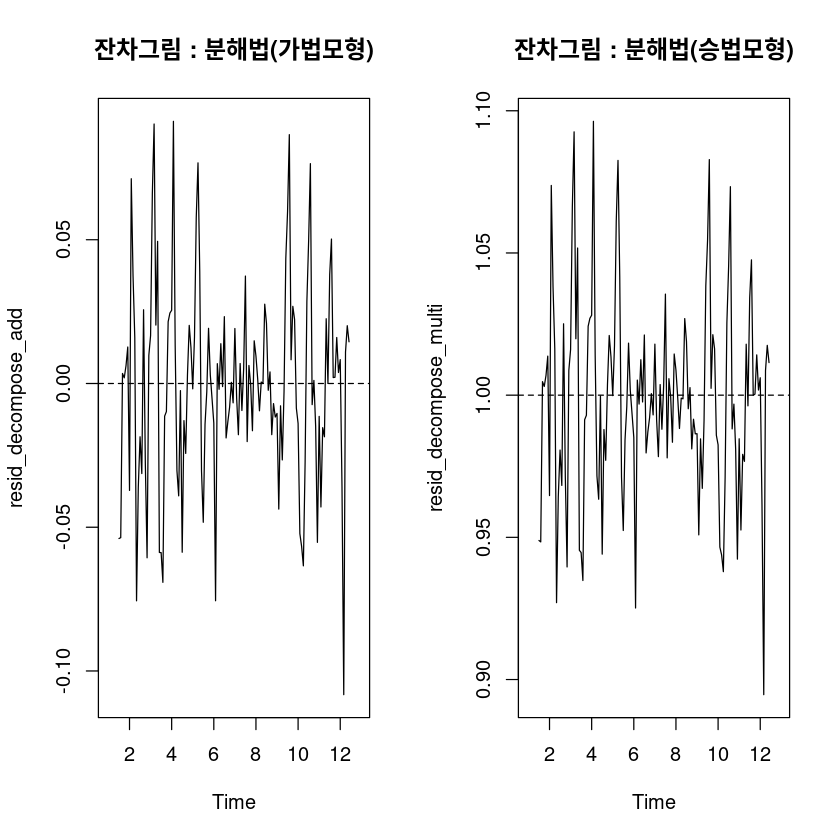

<- m_decompose_add$ random<- m_decompose_multi$ randompar (mfrow= c (1 ,2 ))plot.ts (resid_decompose_add, main= "잔차그림 : 분해법(가법모형)" )abline (h= 0 , lty= 2 )plot.ts (resid_decompose_multi, main= "잔차그림 : 분해법(승법모형)" )abline (h= 1 , lty= 2 )

t.test (resid_decompose_add)t.test (resid_decompose_multi, mu= 1 )

One Sample t-test

data: resid_decompose_add

t = -0.28335, df = 131, p-value = 0.7774

alternative hypothesis: true mean is not equal to 0

95 percent confidence interval:

-0.006909609 0.005178249

sample estimates:

mean of x

-0.00086568

One Sample t-test

data: resid_decompose_multi

t = -0.59098, df = 131, p-value = 0.5556

alternative hypothesis: true mean is not equal to 1

95 percent confidence interval:

0.992186 1.004219

sample estimates:

mean of x

0.9982026

t-test 결과 가법모형에서 예측오차의 평균은 0이라고 할 수 있고, 승법모형에서 예 측오차의 평균은 1이라고 할 수 있다

:: dwtest (lm (resid_decompose_add~ 1 ), alternative= "two.sided" ):: dwtest (lm (resid_decompose_multi~ 1 ), alternative= "two.sided" )

Durbin-Watson test

data: lm(resid_decompose_add ~ 1)

DW = 1.1441, p-value = 7.258e-07

alternative hypothesis: true autocorrelation is not 0

Durbin-Watson test

data: lm(resid_decompose_multi ~ 1)

DW = 1.1426, p-value = 6.946e-07

alternative hypothesis: true autocorrelation is not 0

DW test 결과 가법,승법 모두 예측오차들 간의 자기 상관이 있는 것으로 보인다.

(5)

주의 : 예측오차의 제곱합을 구하기 위해서는 로그변환한 자료를 사용한 분석 방법 의 경우 지수함수를 이용한 역변환을 한 후 계산해야 한다.

<- z- exp (fitted (m_trend)) #추세모형을 적합한 경우의 예측오차 <- z[- (1 : 12 )]- exp (m_smoothing$ fitted[,1 ]) #평활(가법)을 적합한 경 <- z[- (1 : 12 )]- m_smoothing_multi$ fitted[,1 ] #평활(가법)을 적합한 <- z - exp (fitted_dec_add) #분해법(가법)을 적합한 경우의 예측오차 <- z - fitted_dec_multi #분해법(승법)을 적합한 경우의 예측오차

#SSE <- sum (e_trend^ 2 , na.rm= T)<- sum (e_smoothing_add^ 2 , na.rm= T)<- sum (e_smoothing_multi^ 2 , na.rm= T)<- sum (e_decompose_add^ 2 , na.rm= T)<- sum (e_decompose_multi^ 2 , na.rm= T)

paste0 ("추세분석에서의 SSE = " , sse1)paste0 ("가법 계절평활법에 의한 SSE = " , sse2)paste0 ("승법 계절평활법에 의한 SSE = " , sse3)paste0 ("가법 분해법에 의한 SSE = " , sse4)paste0 ("승법 분해법에 의한 SSE = " , sse5)

'추세분석에서의 SSE = 49268.5277996137'

'가법 계절평활법에 의한 SSE = 20103.3932111226'

'승법 계절평활법에 의한 SSE = 20138.5987482274'

'가법 분해법에 의한 SSE = 15284.0239261845'

'승법 분해법에 의한 SSE = 14748.922939659'

#MSE <- mean (e_trend^ 2 , na.rm= T)<- mean (e_smoothing_add^ 2 , na.rm= T)<- mean (e_smoothing_multi^ 2 , na.rm= T)<- mean (e_decompose_add^ 2 , na.rm= T)<- mean (e_decompose_multi^ 2 , na.rm= T)

paste0 ("추세분석에서의 MSE = " , mse1)paste0 ("가법 계절평활법에 의한 MSE = " , mse2)paste0 ("승법 계절평활법에 의한 MSE = " , mse3)paste0 ("가법 분해법에 의한 MSE = " , mse4)paste0 ("승법 분해법에 의한 MSE = " , mse5)

'추세분석에서의 MSE = 342.142554163984'

'가법 계절평활법에 의한 MSE = 152.298433417596'

'승법 계절평활법에 의한 MSE = 152.565142032026'

'가법 분해법에 의한 MSE = 115.788060046852'

'승법 분해법에 의한 MSE = 111.734264694387'

MSE 역시 승법 분해법을 이용했을 때 가장 작은 값을 갖는다